Monte Carlo Simulation شرح : Monte Carlo Simulation - Econowmics - Monte carlo simulations are an incredibly powerful tool in numerous contexts, including operations research, game theory, physics, business and once we run the monte carlo simulation for several stocks, we may want to calculate the probability of our investment having a positive return, or 25.

Monte Carlo Simulation شرح : Monte Carlo Simulation - Econowmics - Monte carlo simulations are an incredibly powerful tool in numerous contexts, including operations research, game theory, physics, business and once we run the monte carlo simulation for several stocks, we may want to calculate the probability of our investment having a positive return, or 25.. Monte carlo simulations are used to model the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random variables. A monte carlo method is a technique that involves using random numbers and probability to solve problems. Monte carlo simulation is a computerized mathematical technique that allows people to account for risk in quantitative analysis and decision making. The expected result depends on how many trials you do. Who uses monte carlo simulation?

You can identify the impact of risk and uncertainty in forecasting models. Ulam and nicholas metropolis in reference to games of. The negative sign problem in quantum monte carlo. I went forward in time. A monte carlo method is a technique that involves using random numbers and probability to solve problems.

Stochastic Simulation and Monte Carlo Methods ... from i.thenile.io The monte carlo simulation is a quantitative risk analysis technique used in identifying the risk level of achieving objectives. The negative sign problem in quantum monte carlo. We will use 5% as the tolerance of v4. We will start the monte carlo simulation using ltspice by of course opening your ltspice software. Monte carlo simulation is not universally accepted in simulating a system that is not in. Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. To do this the computer program must generate random numbers from a uniform distribution. Random outcomes are central to the technique, just as they are to roulette and slot machines.

One of the lessons of doing monte carlo simulation to estimate probabilities is to have a sufficiently high sample count to get a good estimate.

Who uses monte carlo simulation? The negative sign problem in quantum monte carlo. Monte carlo methods are often used when simulating physical and mathematical systems. Monte carlo simulation is a process of running a model numerous times with a random selection from the input distributions for each variable. Our circuit model in this monte carlo simulation is a comparator as shown in figure 1 below. Other performance or statistical outputs are indirect methods which depend on the applications. National laboratory originally used it to model the random diffusion of 1. Where the probability of different. Monte carlo simulations are used to model the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random variables. One of the lessons of doing monte carlo simulation to estimate probabilities is to have a sufficiently high sample count to get a good estimate. Monte carlo simulation was developed as part of the atomic program. Monte carlo simulations model the probability of different outcomes in forecasts and estimates. We will use 5% as the tolerance of v4.

Monte carlo simulations have come a long way since they were initially applied in the 1940s when scientists working on the atomic bomb calculated the probabilities of one to create a monte carlo simulation, you need a quantitative model of the business activity, plan, or process you wish to explore. The negative sign problem in quantum monte carlo. Nasa.gov brings you the latest images, videos and news from america's space agency. This method is applied to risk quantitative analysis and decision making problems. We will use 5% as the tolerance of v4.

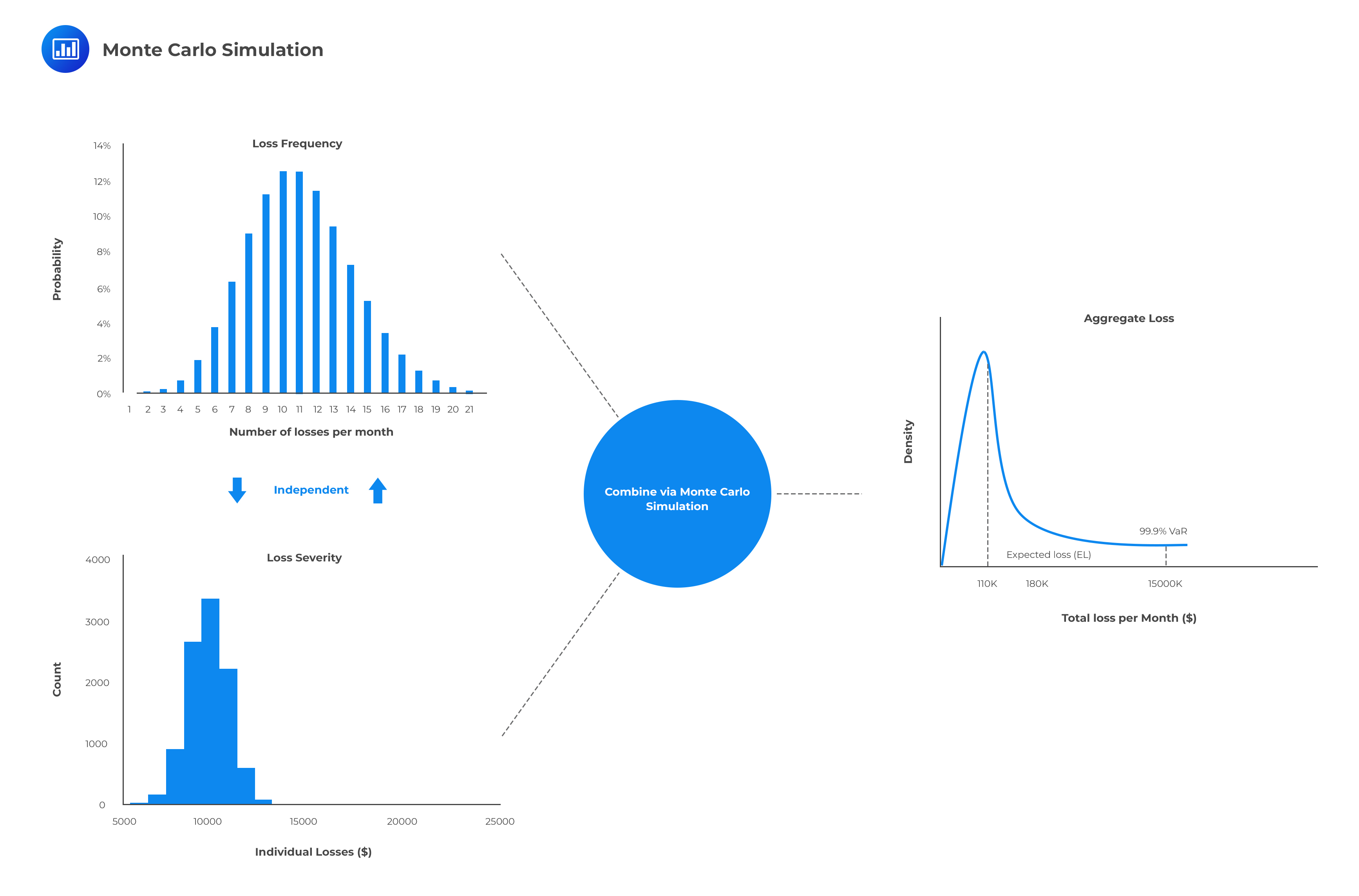

Operational Risk - FRM Study Notes | FRM Part 1 & 2 ... from cdn.analystprep.com You can identify the impact of risk and uncertainty in forecasting models. Monte carlo simulation is a process of running a model numerous times with a random selection from the input distributions for each variable. As an example of how simulation works consider an example. A monte carlo method is a technique that involves using random numbers and probability to solve problems. How can you simulate values of a discrete random variable? One of the lessons of doing monte carlo simulation to estimate probabilities is to have a sufficiently high sample count to get a good estimate. How does it related to the monte carlo method? If you can program, even just a little, you can write a monte carlo simulation.

The monte carlo algorithm relies on repeated random sampling to derive numerical results, and the simulator predicts results giving users a better chance of mitigating risks.

The negative sign problem in quantum monte carlo. Monte carlo simulations and error analysis. The monte carlo algorithm relies on repeated random sampling to derive numerical results, and the simulator predicts results giving users a better chance of mitigating risks. How does it related to the monte carlo method? Ulam and nicholas metropolis in reference to games of. Implementing a powerful statistical tool from scratch. Monte carlo simulation must emulate the chance variations that affect system performance in real life. Monte carlo simulation is a statistical method applied in financial modelingwhat is financial modelingfinancial modeling is performed in excel to forecast a company's financial performance. Our circuit model in this monte carlo simulation is a comparator as shown in figure 1 below. This technique was invented by an atomic nuclear scientist named stanislaw ulam in 1940, it was named monte carlo after the city in monaco that is famous for casinos. You can identify the impact of risk and uncertainty in forecasting models. Monte carlo simulation was developed as part of the atomic program. Where the probability of different.

What happens when you type =rand() in a cell? Scientist at the los alamos. Get the latest updates on nasa missions, watch nasa tv live, and learn about our quest to reveal the unknown and benefit all humankind. Monte carlo error analysis 5. What is a monte carlo simulation?

6. Monte Carlo Simulation (With images) | Computational ... from i.pinimg.com If you can program, even just a little, you can write a monte carlo simulation. Ulam and nicholas metropolis in reference to games of. Where the probability of different. Monte carlo simulation is a powerful tool for approximating a distribution when deriving the exact one is difficult. Monte carlo simulations and error analysis. Recall the following dialogue in the 2019 blockbuster avengers: What is monte carlo simulation? Monte carlo simulation is not universally accepted in simulating a system that is not in.

What is monte carlo simulation?

Monte carlo simulations are an incredibly powerful tool in numerous contexts, including operations research, game theory, physics, business and once we run the monte carlo simulation for several stocks, we may want to calculate the probability of our investment having a positive return, or 25. Get the latest updates on nasa missions, watch nasa tv live, and learn about our quest to reveal the unknown and benefit all humankind. Nasa.gov brings you the latest images, videos and news from america's space agency. Monte carlo simulation is a process of running a model numerous times with a random selection from the input distributions for each variable. Monte carlo simulation is a statistical method applied in financial modelingwhat is financial modelingfinancial modeling is performed in excel to forecast a company's financial performance. Monte carlo simulations model the probability of different outcomes in forecasts and estimates. The expected result depends on how many trials you do. One of the lessons of doing monte carlo simulation to estimate probabilities is to have a sufficiently high sample count to get a good estimate. To do this the computer program must generate random numbers from a uniform distribution. Monte carlo simulations are techniques which approximate solutions to problems through statistical sampling. Monte carlo simulation was developed as part of the atomic program. Where the probability of different. We will start the monte carlo simulation using ltspice by of course opening your ltspice software.

A monte carlo simulation is a randomly evolving simulation monte carlo!. 'monte carlo simulation' is used for propagating (translating) uncertainties present in model inputs into uncertainties in model outputs (results).

0 Komentar